Trust Basics

Whether you’re seeking to manage your own assets, control how your assets are distributed after your death, or plan for incapacity, trusts can help you accomplish your estate planning goals. Their power is in their versatility–many types of trusts exist, each designed for a specific purpose. Although trust law is complex and establishing a trust requires the services of an experienced attorney, mastering the basics isn’t hard.

What is a trust?

A trust is a legal entity that holds assets for the benefit of another. Basically, it’s like a container that holds money or property for somebody else. There are three parties in a trust arrangement:

- The grantor (also called a settlor or trustor): The person(s) who creates and funds the trust

- The beneficiary: The person(s) who receives benefits from the trust, such as income or the right to use a home, and has what is called equitable title to trust property

- The trustee: The person(s) who holds legal title to trust property, administers the trust, and has a duty to act in the best interest of the beneficiary

You create a trust by executing a legal document called a trust agreement. The trust agreement names the beneficiary and trustee, and contains instructions about what benefits the beneficiary will receive, what the trustee’s duties are, and when the trust will end, among other things.

Funding a trust

You can put almost any kind of asset in a trust, including cash, stocks, bonds, insurance policies, real estate, and artwork. The assets you choose to put in a trust will depend largely on your goals. For example, if you want the trust to generate income, you should put income-producing assets, such as bonds, in your trust. Or, if you want your trust to create a fund that can be used to pay estate taxes or provide for your family at your death, you might fund the trust with a life insurance policy.

Potential trust advantages:

- Minimize estate taxes

- Shield assets from potential creditors

- Avoid the expense and delay of probate

- Preserve assets for your children until they are grown (in case you should die while they are still minors)

- Create a pool of investments that can be managed by professional money managers

- Set up a fund for your own support in the event of incapacity

- Shift part of your income tax burden to beneficiaries in lower tax brackets

- Provide benefits for charity

Potential trust disadvantages

- There are costs associated with setting up and maintaining a trust, which may include trustee fees, professional fees, and filing fees

- Depending on the type of trust you choose, you may give up some control over the assets in the trust

- Maintaining the trust and complying with recording and notice requirements can take considerable time

- Income generated by trust assets and not distributed to trust beneficiaries may be taxed at a higher income tax rate than your individual rate

Types of trusts

There are many types of trusts, the most basic being revocable and irrevocable. The type of trust you should use will depend on what you’re trying to accomplish.

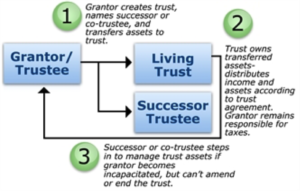

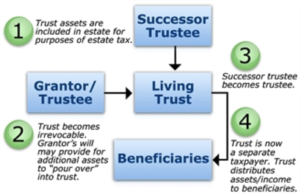

Living (revocable) trust

A living trust is a trust that you create while you’re alive.

A living trust:

- Avoids probate: Unlike property that passes to heirs by your will, property that passes by a living trust is not subject to probate, avoiding the delay of property transfers to your heirs and keeping matters private

- Maintains control: You can change the beneficiary, the trustee, any of the trust terms, move property in or out of the trust, or even end the trust and get your property back at any time

- Protects against incapacity: If because of an illness or injury you can no longer handle your financial affairs, a successor trustee can step in and manage the trust property for you while you get better. In the absence of a living trust or other arrangement, your family may have to ask the court to appoint a guardian to manage your property

A living trust can also continue after your death–you can direct the trustee to hold trust property until the beneficiary reaches a certain age or gets married, for instance.

Despite the benefits, living trusts have some drawbacks. Property in a living trust is generally not protected from creditors, and you cannot avoid estate taxes using a living trust.

Irrevocable trusts

Unlike a revocable trust, you can’t easily change or revoke an irrevocable trust. You usually cannot change beneficiaries or change the terms of the trust. Irrevocable trusts are frequently used to minimize potential estate taxes. The transfer may be subject to gift tax at the time property is transferred into the trust, but the property, plus any future appreciation, is usually removed from your gross estate.

Additionally, property transferred through an irrevocable trust will avoid probate, and may be protected from future creditors.

Whether you’re seeking to manage your own assets, control how your assets are distributed after your death, or plan for incapacity, trusts can help you accomplish your estate planning goals. For more information, consult an experienced attorney.

Copyright 2006- Broadridge Investor Communication Solutions, Inc. All rights reserved.

*Non-deposit investment products and services are offered through Sorrento Pacific Financial, LLC (“SPF”), a registered broker-dealer (Member FINRA / SIPC) and SEC Registered Investment Advisor. Products offered through SPF: are not FDIC or otherwise federally insured, are not a deposit or guarantee of the bank, and may involve investment risk including possible loss of principal. Investment Representatives are registered through SPF. The Bank has contracted with SPF to make non-deposit investment products and services available to bank clients.

Financial Consultants are registered to conduct securities business and licensed to conduct insurance business in limited states. Response to, or contact with, residents of other states will be made only upon compliance with applicable licensing and registration requirements. The information in this website is for U.S. residents only and does not constitute an offer to sell, or a solicitation of an offer to purchase brokerage services to persons outside of the United States.

SPF representatives do not provide tax or legal guidance. For such guidance please consult with a qualified professional. Information shown is for general illustration purposes and does not predict or depict the performance of any investment or strategy. Past performance does not guarantee future results.

{kind=link}